What is CIBIL Dispute?

CIBIL Dispute is the process of identifying and fixing errors in your credit report or The process of finding and resolving inaccuracies in your credit report is called CIBIL Dispute.

The primary credit bureau in the country, Credit Information Bureau India Limited, or CIBIL, is responsible for gathering and assessing consumer credit information. This entails obtaining client credit data and applying several factors to determine each customer's credit score. It is customary for businesses as well as individual consumers to assign credit scores and record credit histories.

A credit bureau assigns a three-digit number known as a CIBIL score. The figure establishes your creditworthiness in terms of money. Before granting you a loan, banks and lenders consider this, which is based on your credit history. When information is gathered from various lenders, TransUnion CIBIL verifies its authenticity before printing it on credit reports. You can always make the necessary corrections if there are any inconsistencies in your CIBIL report or score, including information about your identity, outstanding balance, date of birth, bank, or loan account.

Types of Disputes that May Arise with CIBIL

Various types of disputes may arise in an individual's or a company's credit report. Knowing the category of dispute makes the process of resolution easier. Here are some of the most prominent dispute types that customers can have with respect to their CIBIL report.

Dispute Category | Applicable To | Detailed Scope of the Dispute (as per CIBIL) |

Personal Information Dispute | Individual (Consumer) | Covers inaccuracies in personal identification details appearing in the consumer credit report, such as name, date of birth, PAN and other identifying particulars maintained by CIBIL and reported by member institutions. |

Contact Information Dispute | Individual (Consumer) | Relates to incorrect or outdated communication details including residential address, office address, phone number or other contact details reflected in the credit information report. |

Employment Information Dispute | Individual (Consumer) | Applies where employment-related information reported in the credit report is incorrect, incomplete or outdated as received from lenders. |

Account Information Dispute | Individual (Consumer) | Includes disputes related to loan or credit card account details such as account type, ownership, current balance, credit limit, repayment status, overdue amount, days past due, account status, write-off or settlement information. |

Ownership Dispute (Consumer) | Individual (Consumer) | Raised when a credit account shown in the consumer credit report does not belong to the individual or has been wrongly linked to their PAN or identity. |

Duplicate Account Dispute (Consumer) | Individual (Consumer) | Applies when the same loan or credit card account appears more than once in the consumer credit report. |

Enquiry Information Dispute | Individual (Consumer) | Covers disputes relating to credit enquiries that are incorrectly recorded, duplicated or not recognised by the consumer in their credit report. |

Company / Account Details Dispute | Company / Commercial Entity | Covers inaccuracies in the Company Credit Information Report (CCR), including company name, legal constitution, registered address, PAN, credit facilities, sanctioned amount, current balance, asset classification, bank remarks, branch details, relationship and status. |

Promoter / Director / Partner Details Dispute | Company / Commercial Entity | Applies to incorrect reporting of promoter, director, proprietor or partner details linked to the company credit profile. |

Ownership Dispute (Company) | Company / Commercial Entity | Raised when a credit facility appearing in the CCR does not belong to the company or is incorrectly mapped to it. |

Duplicate Account Dispute (Company) | Company / Commercial Entity | Applies where the same credit facility or account is reported more than once in the company credit report. |

Suit / Legal Information Dispute | Company / Commercial Entity | Covers incorrect reporting of suit-filed information, wilful defaulter classification or related legal data reflected in the CCR. |

Delayed Dispute Resolution (Compensation Framework) | Individual and Company | Applies when a valid dispute raised with CIBIL is not resolved within 30 calendar days. As per the compensation framework, compensation becomes payable for each day of delay beyond the prescribed timeline. |

How Can you Raise a Dispute on the CIBIL Website?

The following steps discuss in detail the procedure to raise a CIBIL dispute online:

Step 1: Access the CIBIL Dispute Resolution PlatformTo raise a dispute, an individual or a company must approach TransUnion CIBIL through the official dispute resolution facilities available on the CIBIL website. CIBIL provides separate dispute resolution mechanisms depending on whether the credit report belongs to an individual consumer or a company, ensuring that disputes are routed through the appropriate channel.

Step 2: Step 2: Identify the Information to be DisputedBefore submitting a dispute, the user is required to clearly identify the incorrect or disputed information appearing in the credit report. The disputed information may relate to personal, contact/employment details, loan/credit facility information, ownership/duplicate accounts, enquiry details, or, in the case of company credit reports, company particulars, promoter/ director details, and legal or suit-related information. Only information that already appears in the credit report can be disputed through CIBIL’s dispute resolution process.

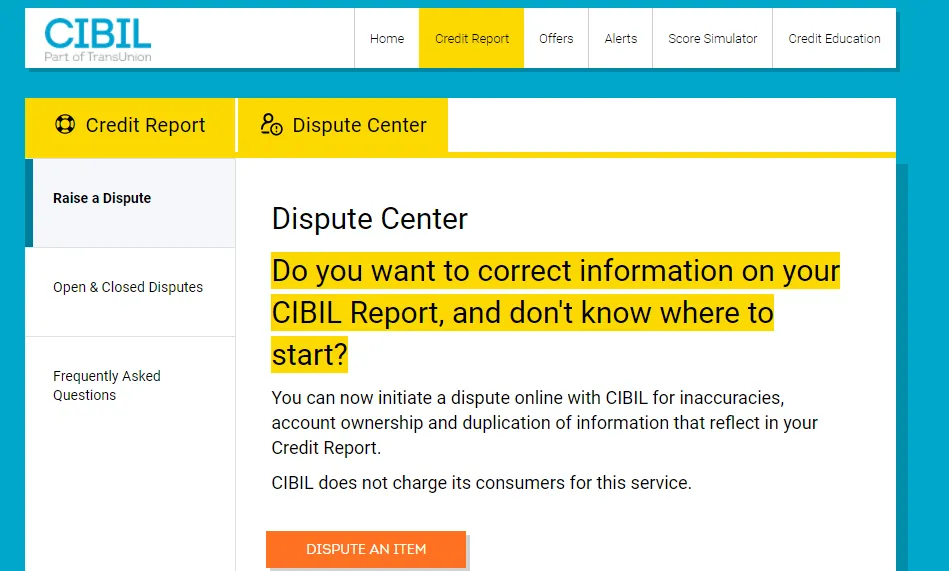

After you log in, click on 'Credit Reports' and select 'Dispute Centre'. Select 'Dispute an Item'.

Step 3: Submit the Dispute Request OnlineThe dispute is raised by submitting a request through the relevant CIBIL dispute interface available on the website. Consumers submit disputes against their Consumer Credit Information Report, while companies submit disputes against their Company Credit Information Report (CCR). During submission, each disputed field or credit account must be selected and included as part of the dispute request.

Fill in the dispute form with your contact details and click on 'Submit'

Step 4: Forwarding of the Dispute to the Credit Institution

Once the dispute request is successfully lodged, CIBIL forwards the disputed information to the concerned credit institution, such as a bank or financial institution, that originally reported the data. CIBIL does not independently alter or correct credit information, as any modification can be carried out only by the reporting member institution after verification.

Step 5: Verification by the Credit Institution

The reporting credit institution reviews the dispute and verifies the disputed information against its internal records. If the institution finds the dispute to be valid, it submits the corrected information to CIBIL. If the dispute is not accepted after verification, the information continues to remain unchanged in the credit report.

Step 6: Update of the Credit Information Report

After receiving the response from the credit institution, CIBIL updates the credit information report based on the verification outcome. The revised information, if any, is then reflected in the individual’s or company’s credit report.

Step 7: Resolution Timeline

As per CIBIL’s dispute resolution process, disputes are required to be resolved within a period of 30 calendar days from the date on which the dispute is submitted.

Step 8: Compensation for Delay, if Applicable

If a dispute is not resolved within the prescribed 30 day timeline, the affected consumer or company becomes eligible for compensation under CIBIL’s Framework for Compensation. Compensation is payable at Rs.100 per day for each day of delay beyond the 30 (calendar) day period, subject to the conditions specified in the framework.

How Can you Raise a CIBIL Dispute Offline?

Follow the instructions given below to raise a CIBIL dispute offline:

Step 1: Identify the Disputed Information

The consumer or company must first identify the incorrect or disputed information appearing in the Consumer Credit Information Report or the Company Credit Information Report. Only information already reflected in the credit report can be disputed.

Step 2: Prepare a Written Dispute Request

Unlike the online method where disputes are raised through CIBIL’s online dispute portal, the offline method requires a written dispute application clearly mentioning the details being disputed, such as personal information, account details, ownership or duplicate accounts, enquiry details, or company and legal information.

Step 3: Send the Written Dispute to CIBIL

The written dispute request must be sent to TransUnion CIBIL at its registered office address:

TransUnion CIBIL Limited

One World Centre, Tower 2A, 19th Floor

Senapati Bapat Marg, Elphinstone Road

Mumbai – 400013, Maharashtra, India

Step 4: Forwarding to the Reporting Credit Institution

After receiving the offline dispute, CIBIL forwards the disputed information to the concerned credit institution that originally reported the data. CIBIL does not make corrections on its own.

Step 5: Verification and Update

The credit institution verifies the disputed information and, if found valid, submits corrected data to CIBIL. CIBIL updates the credit report based on the lender’s response.

Step 6: Timeline and Compensation

Disputes raised offline are required to be resolved within 30 calendar days. If there is a delay beyond this period, compensation becomes payable under the Framework for Compensation at Rs.100 per day for each day of delay beyond 30 days, subject to applicable conditions.

How to Resolve CIBIL Disputes?

This stepwise resolution process explains how CIBIL handles, verifies, and updates the disputed information after it has been submitted:

Step 1: Raising the Dispute: The consumer or company identifies incorrect or outdated information in their credit report and submits a dispute using CIBIL’s official dispute resolution mechanism, either online or offline.

Step 2: Forwarding to the Reporting Institution: CIBIL forwards the disputed information to the concerned bank or financial institution that originally reported the data. CIBIL itself does not modify or correct information.

Step 3: Verification by the Lender: The reporting institution verifies the disputed details against its records. If an error is confirmed, the lender submits the corrected information back to CIBIL. If the dispute is not valid, the information remains unchanged.

Step 4: Updating the Credit Report: After receiving the verified response from the lender, CIBIL updates the consumer’s or company’s credit report accordingly, reflecting any corrections.

Step 5: Timeline and Compensation: The dispute must be resolved within 30 calendar days from submission. If this timeline is exceeded, the consumer or company becomes eligible for compensation under the Framework for Compensation at Rs. 100 per day for each day of delay beyond 30 days.

How to Register a Complaint on CIBIL’s Consumer Dispute Resolution Portal?

Here are the steps to register a complaint on CIBIL’s Consumer Dispute Resolution portal:

- Log into CIBIL Dashboard using your credential

- To check the updated version of CIBIL report by refreshing your report

- To register your complaint, fill in the dispute request form

- If required, you need to fill in multiple forms

- Your complaint will be raised by the TransUnion CIBIL by reaching out to the lenders

- The required changes will be reflected on the CIBIL report within 30 days of raising the complaint.

What are Credit Reports?

Credit history, including loan and credit card payments, is monitored by the Credit Information Bureau (India) Limited (CIBIL). Each month, CIBIL produces Credit Information Reports (CIR) and credit ratings based on data from different banks and other financial organisations. In order to assess a person's capacity to repay loans, banks typically look at their credit history. If your credit score is high, the bank is more likely to approve your loan. CIBIL typically yields a three-digit score. Consumers with credit scores ranging from 300 to 900 are eligible.

Documents Required for Visiting the CIBIL Office

The following is the list of documents required by the consumers for visiting the CIBIL Office:

Entity Type | Required Documents (as per CIBIL links) |

Individual Customers | Proof of identity such as PAN, Driving License, Passport, or Voter ID. |

Corporate Entities (Private & Public Limited Companies) | Identity proof of the authorised signatory (PAN, Driving License, or Passport) submitting the request; entity details as per the Company Credit Information Report (CCR) request. |

Other Entities (General Guidance) | For any other entity (e.g., Trust, Partnership Firm, HUF, Government Bodies), the authorised signatory’s identity proof is required. If the entity has its own PAN, it may be submitted where available. |

CIBIL Customer Care Details

Here are the details of CIBIL customer care details:

Particulars | Official Details from CIBIL Links |

Registered Corporate Office Address | TransUnion CIBIL Limited, One World Centre, Tower 2A, 19th Floor, Senapati Bapat Marg, Elphinstone Road, Mumbai – 400 013, Maharashtra, India. |

Consumer Helpline Number | +91 22 6140 4300 (Monday to Saturday, 10:00 am – 6:00 pm). |

Email ID for General Queries | CIBILinfo@transunion.com. |

Fax (if needed) | +91 22 6638 4666 |

Contact Form / Online Support | Accessible via CIBIL’s contact pages on cibil.com or transunioncibil.com. |

How to Dispute Errors in Credit Report?

A detailed process on how you can dispute errors in credit report is mentioned below -

- Step 1: Submit Your Dispute Online

- Visit CIBIL’s dispute resolution section and fill in the online dispute form to report incorrect information in your credit report. Choose the exact field or account you want to dispute and enter the control number mentioned on your credit report before submitting.

- Step 2: Wait for Verification

- Once you submit the dispute, CIBIL shares the details with the concerned bank or financial institution for verification. CIBIL does not make changes on its own.

- Step 3: Check Your Updated Credit Report

- After verification, the information is either corrected or retained based on the lender’s response. The updated status is reflected in your credit report. Disputes are resolved within 30 calendar days from the date of submission.

Disclaimer

Display of any trademarks, tradenames, logos and other subject matters of intellectual property belong to their respective intellectual property owners. Display of such IP along with the related product information does not imply BankBazaar's partnership with the owner of the Intellectual Property or issuer/manufacturer of such products.

How Can you Raise a Dispute on the CIBIL Website?

If you want to raise a CIBIL dispute offline, you can always write to TranUnion CIBIL:

TransUnion CIBIL Limited,

One Indiabulls Centre, Tower 2A, 19th Floor,

Senapati Bapat Marg, Elphinstone Road,

Mumbai - 400 013

Step 1

Go to the website and click on 'myCIBIL' and log into CIBIL

Step 2

After you log in, click on 'Credit Reports' and select 'Dispute Centre'. Select 'Dispute an Item'.

Step 3

Fill in the dispute form with your contact details and click on 'Submit'

FAQs on CIBIL disputes in India

1.What are the various situations in which I can raise a CIBIL dispute?

A CIBIL dispute can be raised in the following events-Inaccurate balance overdue, Inaccurate personal details, and Ownership issues

2.Why does CIBIL not confirm information with customers before drawing the CIBIL report?

CIBIL looks up to various credit institutions for furnishing accurate information. Customer involvement in this case is neither required nor advisable.

3.What should I do when I see an error in my CIBIL report?

Any error in your CIBIL report should immediately be informed and rectified. For this the first step would be to fill out the online dispute form at the CIBIL official website.

4.How do I know that my dispute with CIBIL has been resolved?

CIBIL sends across an email as well as SMS for letting you know that your dispute has been resolved.

5.What do I do if I am not satisfied with the dispute resolution?

In case, you are dissatisfied with the dispute resolution, you will need to raise a new request or contact CIBIL directly. CIBIL updates report on only when it is furnished by the credit institutions.

6.Is there any way I can personally visit the CIBIL office to raise a dispute?

No. CIBIL disputes can be raised only via CIBIL's website and application form for the same can also be filled online. Tracking the dispute request happens via email as well as SMS.

CIBIL Score Requirements for Loans

Disclaimer

Credit Card:

Credit Score:

Personal Loan:

Home Loan:

Fixed Deposit:

Copyright © 2026 BankBazaar.com.